Franchising, retail, business

29/09/2015

Joining the Eurozone was once a near unquestionably good idea. Now, the costs of joining the monetary union are under close scrutiny.

This column takes a slightly different tack, presenting an alternative perspective on how joining the euro has impacted productivity in southern Europe. It turns out that capital wasn’t allocated efficiently across firms after cheap borrowing at low interest rates, impacting total factor productivity.

Source: VOXEU – Gita Gopinath, Sebnem Kalemli-Ozcan, Loukas Karabarbounis, Carolina Villegas-Sanchez 28 September 2015

The ongoing Greek debt crisis has renewed interest among economists and policymakers in understanding the costs associated with joining the Eurozone. It has also generated concerns that countries in Southern Europe could have been better off if they had never joined in the first place. Partly, these concerns arise from the fact that countries in the south were able to borrow at lower interest rates in the run up to and following the introduction of the euro. As creditors deemed these countries less risky than before and as the ECB strengthened its anti-inflationary policy, borrowing rates decreased and these economies experienced large inflows of capital (Feldstein 2012).

While borrowing rates have converged among countries in the Eurozone, productivity growth rates have actually diverged. Countries in the South experienced lower productivity growth than other European countries. There is some work suggesting that part of the lower productivity growth in Southern Europe is related to the boom in the construction sector and the shift of resources from traded to non-traded sectors (Reis 2013, Benigno and Fornaro 2014).

In recent work (Gopinath et al. 2015), we highlight an alternative (but complementary) view of how the euro convergence process may have impacted productivity in Southern Europe. We argue that, following the lowering of interest rates, capital was not allocated efficiently across firms in the South. In turn, the misallocation of capital flows generated declines in total factor productivity.

There are two aspects of our work that are of particular relevance when thinking about capital allocation and productivity in Southern Europe over the past two decades. First, we tie dynamics in measures of misallocation to the evolution of productivity and capital flows over time. The pioneering work of Restuccia and Rogerson (2008) and Hsieh and Klenow (2009) provides the intellectual basis for understanding the implications of resource misallocation on aggregate outcomes. Second, we develop a framework that allows us to relate financial frictions at the firm level to the misallocation of capital across firms and its evolution over time. The potential of financial frictions to generate misallocation of capital has been emphasised by previous work (Kiyotaki and Moore 1997, Banerjee and Duflo 2005). However, lacking good data on both firm-level financial and production decisions, evidence on the importance of financial frictions for the misallocation of capital has been scant.

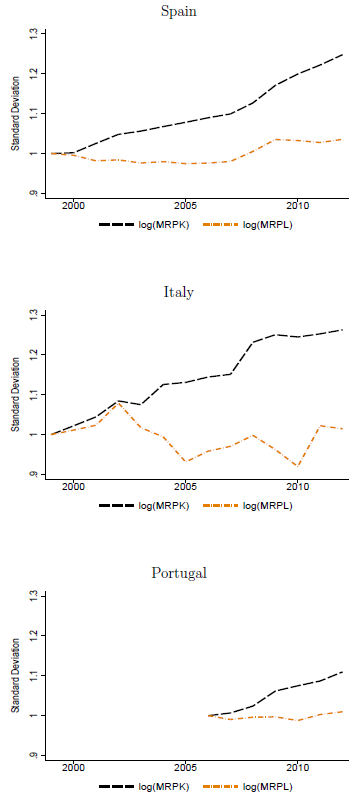

We use a large and nationally representative dataset of manufacturing firms between 1999 and 2012 that contains information on both financial and production decisions to document three key facts. First, the dispersion of the return to capital across firms increased significantly in Spain, Italy, and Portugal. Second, the dispersion of the return to labour did not change significantly over time. Figure 1 plots the dispersion of the returns to capital and labour over time, where we measure dispersion as the within four-digit sector standard deviation. Last but not least, the increasing dispersion of the return to capital in these countries was in some cases accompanied by significant productivity losses.

The efficient accumulation of capital

How to interpret these facts? We start with the observation that frictions impeding the efficient accumulation of capital are likely to be important for firms in the South because these firms operate within relatively underdeveloped capital markets. We argue that for these countries, the decline in the interest rate is an important factor explaining the increasing dispersion of capital returns across firms and the productivity losses from misallocation.

The logic of our argument can be understood by first considering the effects of a decline in the interest rate in a world without financial frictions. If firms faced no frictions to their capital accumulation, then the decline in the interest rate would have led capital to be allocated to the most productive investments until all returns were equalised. In this hypothetical world, all firms would face similar returns to capital and, therefore, we would not have observed changes in the dispersion of the return to capital across firms.

Using our large and representative sample of firms, we find that, in reality, capital was increasingly allocated to less productive firms over time. We also document that firms with higher net worth invested more in physical capital and borrowed more than firms with lower net worth but otherwise similar productivity. The dispersion of the return to capital across firms increased because some productive and high-return firms were constrained from increasing their investment. Total factor productivity declined because capital was allocated inefficiently over time.

A standard view of financial markets argues that capital inflows due to a financial market liberalisation increases productivity by leading to a more efficient allocation of capital across firms. An important lesson from our work for economists and policymakers is that capital inflows due to declines in the interest rate may actually impact productivity in a negative way. In an environment with low interest rates, capital can be allocated to less efficient firms if financial markets remain underdeveloped. Financial market imperfections in Southern nations of the Eurozone bear some of the blame for their poor productivity performance.

By lowering interest rates and encouraging an inflow of capital, the adoption of the euro may have been partly responsible for the misallocation of capital and the low productivity observed in the South. While this does not necessarily mean that the adoption of the euro was economically harmful overall, it does highlight one negative consequence through its effect on interest rates when capital markets are relatively underdeveloped. Policymakers concerned with lagging productivity growth in Southern nations would be wise to look for ways to improve the functioning of their financial markets.

Authors’ note: The views expressed herein are those of the authors and not necessarily those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System.

References

Banerjee and Duflo (2005), “Growth Theory Through the Lens of Development Economics”, inHandbook of Economic Growth, 473-552.

Benigno and Fornaro (2014), “The Financial Resource Curse”, Scandinavian Journal of Economics116(1): 58-86.

Feldstein (2012), “The Failure of the Euro”, Foreign Affairs, January-February.

Gopinath, Kalemli-Ozcan, Karabarbounis, and Villegas-Sanchez (2015), “Capital Allocation and Productivity in South Europe”, NBER Working Paper No 21453.

Hsieh and Klenow (2009), “Misallocation and Manufacturing TFP in China and India”, Quarterly Journal of Economics 124(4): 1403-1448.

Kiyotaki and Moore (1997), “Credit Cycles”, Journal of Political Economy 105(2): 211-248.

Reis (2013), “The Portuguese Slump and Crash and the Euro Crisis”, Brookings Papers on Economic Activity 1: 143-210.

Restuccia and Rogerson (2008), “Policy Distortions and Aggregate Productivity with Heterogeneous Plants”, Review of Economic Dynamics 11(4): 707-720.

![]()

![]() L’idea di creare un blog giornaliero per il mondo del retail nasce grazie ai continui feedback positivi che riceviamo dalle notizie condivise attraverso diversi canali.

L’idea di creare un blog giornaliero per il mondo del retail nasce grazie ai continui feedback positivi che riceviamo dalle notizie condivise attraverso diversi canali.

Rivolto a tutte le tipologie di distribuzione presenti sul mercato: dal dettaglio ai grandi mall, dal commercio locale e nazionale alle catene di negozi internazionali, investitori, ai nostri fedeli clienti e chiunque altro è realmente interessato allo studio e all'approfondimento su ciò che guida il comportamento dei consumatori. E' anche un blog per tutti coloro i quali lavorano già nel mondo del Retail.

Verranno condivise le loro esperienze, le loro attitudini e le loro experties. Un blog di condivisione, quindi.

Ospitato sul sito della BRD Consulting, che da decenni lavora nel mondo distributivo Italiano ed Internazionale, il blog Store in & out riguarderà il business, i marchi e i comportamenti d'acquisto propri di alcune delle più grandi aziende.

Ci saranno anche notizie in lingua originale per dare evidenza dell’attenzione della nostra Azienda nei confronti del global.

È possibile raggiungere lo staff a: info@brdconsulting.it

")

")

")

")

")

")